Gambling Payment Processing UK: Complete Guide (2026)

Gambling Payment Processing UK: Complete Guide (2026) Getting paid is the hardest part of running a gambling business in the UK. Not the marketing. Not the licensing. The payments. Most processors won’t touch you. The ones that do charge extortionate rates or shut your account down the moment your chargeback ratio ticks up. Gambling payment processing in the UK is a different beast — and you need to treat it that way. What is Gambling Payment Processing? It’s the system that moves money between your players and your business account. Deposits, withdrawals, refunds — all of it. Sounds simple. It isn’t. How It Differs From Standard Payment Processing A standard ecommerce business applies for a Stripe account and gets approved in minutes. A gambling operator does the same thing and gets rejected before the page even loads. Gambling payment processing sits in a completely different risk category. Higher fraud rates. Higher chargebacks. Regulatory scrutiny from the UKGC. That’s why you need a processor built specifically for this. Offshore Gateways specialises in exactly this – online gambling payment processing for operators who’ve been turned away everywhere else. Why Gambling is Classified as High-Risk in the UK Three reasons. Chargebacks, fraud, and regulation. Players dispute transactions. Sometimes legitimately, sometimes not. Either way, your chargeback ratio climbs — and mainstream processors don’t want that liability anywhere near their books. Why High Street Banks Reject Gambling Merchants Barclays, HSBC, NatWest — they all have blanket policies against gambling merchants. It’s not personal. It’s their risk appetite. A gambling merchant account requires a specialist acquirer. Someone who understands MCC 4722, UKGC compliance, and the difference between a fraud spike and a seasonal volume surge. Still getting rejected by mainstream processors? Offshore Gateways works with gambling operators across the UK. Get approved in 48–72 hours. UK Gambling Payment Regulations – UKGC & FCA Requirements If you’re operating in the UK, you need a UKGC licence. Full stop. Your payment gateway for gambling also needs to comply with FCA guidelines – especially around AML and transaction monitoring. AML and KYC Requirements for Gambling Merchants Every player making significant deposits needs to be verified. Source of funds checks. Identity verification. Transaction monitoring. Your gambling merchant account provider should have this built into their onboarding. If they don’t – walk away. The UKGC will find you before you find the problem. How Gambling Payment Processing Works Player hits deposit. Enters card details. Gateway authenticates the transaction. Acquirer approves. Funds land in your merchant account. Settlement hits your business account 2-5 days later. That’s the clean version. In practice, gambling payment processing gets more complex – 3D Secure authentication, velocity checks, rolling reserves, and multi-currency conversion all happen in the background. Accepted Payment Methods for Gambling Sites Debit cards (Visa, Mastercard — credit cards banned for gambling in UK since 2020) Open banking payments E-wallets (PayPal, Skrill, Neteller) Crypto (for offshore-licensed operators) Bank transfers for high-value players Multi-Currency Processing for UK Operators If you’re taking players from outside the UK, multi-currency matters. GBP, EUR, USD – your processor needs to handle conversion without killing your margins. Check out Offshore Gateways’ open banking solutions for faster settlement and lower fees on direct bank transfers. iGaming Payment Solutions – Best Options in 2026 The iGaming payment solutions landscape has shifted. Cards are still dominant but open banking is growing fast – lower fees, instant settlement, no chargeback risk on deposits. For UK operators, casino payment processing via open banking is becoming the preferred route for deposits specifically. Open Banking Payments for Gambling Sites Direct bank-to-bank. No card network fees. No fraud disputes on the deposit side. Players authenticate through their banking app – it’s faster than entering card details and converts better. iGaming payment solutions built on open banking also sidestep the UK credit card gambling ban entirely. Worth exploring if you haven’t already. Read more: iGaming Open Banking Payment Challenges – and How to Fix Them Crypto Payment Processing for iGaming For offshore-licensed operators, crypto adds a genuine alternative channel. Bitcoin, Ethereum, stablecoins – processed through a compliant gateway with KYC built in. Online gambling payment processing via crypto is growing in markets where card approval rates are low. Not mainstream yet in the UK, but worth having as a backup channel. How to Get Approved for a Gambling Merchant Account UK Don’t apply to the wrong place. That’s step one. Online gambling payment processing approvals take longer when you apply through a generic processor and get rejected — that rejection history follows you. Documents Required for Approval UKGC operator licence 3–6 months processing history (if available) Business registration documents Director ID and proof of address Website with live terms, privacy policy, and responsible gambling page AML policy document Approval Timeline – What to Expect Clean application with all documents ready – 48 to 72 hours with a specialist. Missing documents or complex ownership structures – 7 to 14 days. Casino payment processing approvals move faster when your website is fully compliant before you apply. Sort the responsible gambling page, the T&Cs, and the refund policy before you hit submit. Stay updated on social media as well – Linkedin Frequently Asked Questions Can UK gambling operators use Stripe or PayPal for payment processing? No. Both block gambling merchants outright. Stripe’s restricted businesses list explicitly excludes gambling. PayPal same story. You need a specialist gambling merchant account through a dedicated high-risk acquirer. What chargeback rate gets a gambling merchant account terminated in the UK? Visa flags you at 0.9% – needs 100+ disputes that month too. Mastercard cuts in at 1.0%. Hit those numbers for a few months running and your Merchant ID is gone. Are credit cards banned for gambling payment processing in the UK? Yes. Banned since April 2020. UKGC rules – no credit cards for gambling transactions, full stop. Debit cards still work. Open banking works. Credit cards don’t. What documents do you need to open a gambling merchant account UK? First off, your UKGC operator licence. You’ll also need: • Director ID + proof of address • 3–6 months processing history • Live website – terms, privacy, responsible gambling page • AML policy doc How

Getting a Merchant Account UK: Online Payment Guide 2026

Getting a Merchant Account UK: Online Payment Guide 2026 Getting paid online sounds simple until you hit a wall of bank rejections, confusing jargon, and zero straight answers from anyone. Let’s cut through it. First – What Even Is a Merchant Account? It’s a holding account. When a customer pays you by card, the money sits there first before hitting your business bank account. Without a merchant account UK, you physically cannot process card payments. That’s it. No account, no revenue. Offshore Gateways works with businesses across the UK who’ve been left hanging by traditional banks – and the number one thing they all say is they wish someone had just explained this properly from day one. Who Actually Needs One? Pretty much any business taking card or online payments needs a merchant account UK. That covers: Online shops and dropshippers Subscription box services Digital product sellers High-risk industries — forex, CBD, gaming, nutraceuticals, adult content If you’re running an ecommerce merchant account, your entire operation depends on this. Customers expect to pay by card. If you can’t take it, you’re losing sales to someone who can. The merchant payment flow only works when this infrastructure is properly set up. Skip it, and you’re stuck. The Step-by-Step Bit (Without the Fluff) Step 1 – Pick the Right Provider Banks aren’t the only option. You’ve got independent processors, specialist offshore acquirers, and payment facilitator companies — each built for different business types. Standard businesses can usually go through a UK high-street bank or a payment facilitator like Stripe or Square. High-risk merchants? You’ll need a specialist. Most mainstream providers will reject you without a second glance. Step 2 – Get Your Docs Together This is where most applications fall apart. Providers need to trust you before they’ll approve a merchant account UK — so bring the evidence. You’ll need: Proof of identity (passport + proof of address for all directors) Certificate of Incorporation and company registration Bank statements – usually 3 to 6 months A live website with clear terms, returns policy, and contact page Processing history if you’ve had accounts before Missing even one of these slows everything down. Step 3 – Apply and Be Honest Fill in the application with accurate numbers. Your actual monthly volume, your real average transaction value, your actual industry. Underestimating your volume to look less risky is one of the most common mistakes — and it backfires badly when the provider notices the mismatch. Real talk: A messy application with gaps and vague answers gets declined. A clean, complete one moves fast. Offshore Gateways has an onboarding team that helps merchants prepare before they even submit — which is why approvals happen quicker. Step 4 – Underwriting and KYC Once submitted, the provider’s team runs checks. AML, KYC, website compliance, chargeback risk — all of it. This is standard for every merchant account UK approval, no matter the provider. Just cooperate quickly when they ask for extra documents and you’ll move through it faster. Step 5 – Integrate and Start Taking Payments After approval, you get your gateway credentials. Most platforms — Shopify, WooCommerce, custom-built sites — can be integrated in a couple of days. Run test transactions first. Then go live. What Does It Cost? Fees vary, but here’s a rough idea of what to expect: Fee Typical Range Per-transaction rate 1.2% – 3.5% Monthly account fee £20 – £100 Chargeback fee £15 – £45 per dispute Setup fee £0 – £500 Rolling reserve (high-risk) 5–10% held for 90–180 days Merchant processing costs more for high-risk industries — but with the right provider, volume-based pricing makes it manageable. Don’t sign anything without understanding every line of the fee schedule. Why Do Applications Get Rejected? It’s almost always one of these: Incomplete documents – don’t rush this part Chargeback rate over 1% – a hard red flag for most providers Vague business description – “digital services” tells a provider nothing Non-compliant website – missing T&Cs or a returns policy kills applications Wrong provider – a high-risk business applying to a standard bank is a waste of time Declined before? That’s not the end. It just means you applied to the wrong place. A specialist payment facilitator with offshore acquiring experience reads your application very differently from a high-street bank. High-Risk Business? Here’s What Opens Up Standard providers won’t touch you. That’s just reality. But a specialist merchant account UK provider – accessed through a company like Offshore Gateways – unlocks a completely different set of options. Things like: Multi-currency processing in 150+ countries Offshore merchant accounts with better approval rates Crypto payment rails for industries where card processing is restricted Open banking for lower-fee direct bank payments An ecommerce merchant account built for high-risk doesn’t just keep the lights on. It lets you grow internationally without constantly worrying about your account getting shut down. Good merchant processing infrastructure is the difference between a business that scales and one that stays stuck. How Long Does All This Take? Low-risk businesses: 3–7 business days from a complete application. High-risk: 7–14 days on average. Some specialist providers fast-track it in 48–72 hours if everything’s in order. The fastest approvals go to merchants who had all their documents ready before hitting submit. Right. Let’s Get You Set Up. You don’t need to spend weeks going back and forth with banks that don’t understand your business model. A proper merchant account UK – with the right provider – is absolutely achievable. You just need someone who knows what they’re doing on your side. Offshore Gateways handles merchant payment solutions for businesses across every risk level. Fast onboarding, real support, no runaround. Get in touch today and let’s get your payments sorted. Stay updated on social media as well – Linkedin Frequently Asked Questions What documents are required to open a UK merchant account? Passport and driving licence for ID. Bank statement or utility bill for address — max 3 months old. You’ll also need your Certificate of Incorporation plus 3–6 months of business bank statements. Does a UK merchant account need FCA authorisation? Not you personally – but your processor does. They must be FCA-registered under the Payment Services Regulations 2017. Check their status on the FCA Register at register.fca.org.uk before committing. Is PCI DSS

Best International Payment Gateway Provider for High-Risk Businesses: 2026 Comparison

International Payment Gateway Provider for High-Risk Businesses If you run a high-risk business, finding the best international payment gateway provider is not just a technical decision – it is a survival decision. Most mainstream processors will reject you, freeze your funds, or shut your account without warning. This guide cuts through the noise and shows you exactly what to look for, who serves this market, and how offshoregateways helps businesses process payments globally without the constant fear of account termination. Why High-Risk Businesses Struggle with Standard Payment Gateways Think of a regular payment gateway like a bank for a normal 9-to-5 worker. It works perfectly – until you show up with an unusual job. Businesses in industries like online gaming, nutraceuticals, forex trading, adult content, travel, and crypto are considered “unusual” by standard processors like Stripe and PayPal. The result? Declined applications. Frozen funds. Sudden account closures. This is where choosing the best international payment gateway provider built specifically for high-risk merchants becomes critical. These specialised providers understand your industry, underwrite your account properly from day one, and give you the payment infrastructure you actually need to grow. What Makes a Payment Gateway “High-Risk Friendly”? Not all payment gateway providers are built the same. A high-risk friendly gateway offers: This list is also exactly what Google wants to show users searching “what does a high-risk payment gateway include” – bookmark it. Best International Payment Gateway Provider Solutions for High-Risk Businesses in 2026 1. offshoregateways – Best Overall for High-Risk Global Businesses Offshoregateways is undoubtedly the most suitable international payment gateway Provider for high-risk businesses. Offshoregateways, with its experience of over 850,000 merchants in 15 years of its existence, is best known for its services to businesses which have been denied access by other payment gateways. What sets it apart: For businesses that need to open offshore merchant account facilities with full compliance and rapid approval, this is the most complete solution available in 2026. 2. Offshore Credit Card Processing Specialists Some payment processing companies focus exclusively on card-not-present transactions for high-risk industries. These providers offer offshore credit card processing infrastructure routed through international acquiring banks in jurisdictions with favourable regulatory environments — such as the EU, Cayman Islands, or Mauritius. The main advantage: your transactions are processed through a bank that has specifically agreed to underwrite your industry, which means dramatically higher approval rates and far fewer account freezes. 3. Cross-Border Payment Gateway Solutions A true cross border payment gateway does more than process cards. It handles currency conversion, local payment methods (Blik, Sofort, WeChat Pay, UPI), tax compliance across jurisdictions, and real-time settlement reporting – all in one dashboard. For businesses selling internationally, this matters enormously. A customer in Germany who sees their local payment method at checkout converts at a significantly higher rate than one forced to enter a foreign credit card. The right cross-border gateway removes that friction entirely. How to Choose the Right Gateway: 5 Questions to Ask Before signing with any provider, ask these five questions: Why 2026 Is the Year to Switch to a Specialist Provider The payments landscape has shifted dramatically. Traditional payment gateway providers are tightening their underwriting. Stripe and PayPal continue to exit high-risk verticals. Meanwhile, global cross-border ecommerce is projected to grow past $8 trillion by 2027. High-risk merchants who lock in a stable, specialist gateway today are building a competitive moat. Those who stay with unstable mainstream processors are one algorithm update away from losing their ability to accept payments entirely. The best international payment gateway provider for your business is not the most famous one – it is the one built for exactly what you do. Conclusion: Stop Settling for Processors That Were Never Built for You Finding the best international payment gateway provider as a high-risk merchant is hard – but it does not have to be. The right provider gives you global reach, multi-currency support, fraud protection, and the kind of stable acquiring relationship that lets you focus on growing your business rather than fighting payment failures. offshoregateways has spent over 15 years building exactly that infrastructure for merchants the mainstream industry ignores. Whether you need to open offshore merchant account facilities, set up offshore credit card processing, or connect to a reliable cross border payment gateway, the solution is already waiting for you. Ready to stop getting rejected and start processing globally? Visit offshoregateways today and speak with a payment specialist within 24 hours. Stay updated on social media as well – Linkedin Frequently Asked Questions Can high-risk businesses get approved for payment processing? Yes. Specialist providers like Offshore Gateways approve high-risk merchants other processors reject, often within 24 to 72 hours. What is an international payment gateway provider? An international payment gateway ensures secure processing of international transactions, allows multiple currencies, and links your business to international acquiring banks. How is an offshore payment gateway different from a regular payment gateway? In an offshore payment gateway, international acquiring banks are used, risky merchants are taken in, multiple currencies are processed, and account stability is superior to those found in regular payment gateways like Stripe and PayPal. What does a rolling reserve in a high-risk merchant account mean? The rolling reserve is a tiny fraction of your daily turnover set aside by the payment processor to cover any risks, which is eventually returned to you after 90 to 180 days. How do I open an offshore merchant account? Apply with a specialist provider, submit your business documents, and get matched with an acquiring bank that accepts your industry. Approval takes 3 to 7 days.

Elementor #27277

iGaming Payment Solutions: Scaling Is Easy, Staying Is Hard

Everyone celebrates the launch. The press releases, the player acquisition numbers, the first big deposit weekend. But ask any operator who has been in this industry for more than two years, and they will tell you the same thing: getting big is the easy part. Staying big is where most brands quietly fall apart. At the heart of that staying power is one thing operators consistently underestimate – their iGaming payment solutions. Offshore Gateways has seen this pattern play out repeatedly, and the operators who thrive long-term are those who treat payment infrastructure not as a backend afterthought, but as a core business function. Why iGaming Feels Easy at First (And Why That’s Dangerous) Think of launching an iGaming brand like building a Lego castle. With the right pieces – a licence, a platform, some game content, a marketing budget — you can have something impressive-looking assembled in a matter of weeks. The danger? Lego castles are easy to knock down. The knocking-down forces in iGaming are predictable: sudden traffic spikes, payment processor pullouts, fraud waves, and shifting regulatory requirements across jurisdictions. None of these destroy operators who are prepared. All of them have destroyed operators who were not. The first place cracks appear is almost always payments. The Three Stages Where iGaming Payment Solutions Fail Operators Stage 1: The Launch Phase (False Confidence) In the beginning, almost any payment setup works. Transaction volumes are low, fraud hasn’t found you yet, and your processor hasn’t noticed your chargeback ratio. Operators at this stage often choose the cheapest or most convenient iGaming payment solutions available. This is the equivalent of building your Lego castle on a glass table. It looks fine – right up until someone bumps into the table. Stage 2: The Growth Phase (Where the Cracks Appear) Growth generates volume, and volume draws attention. Your payment processor starts to get curious. Chargebacks start coming in. There is increased automation for some player locations. All of a sudden, your approvals are down and you do not know why. Operators in this phase discover the hard way that iGaming payment solutions are not all built for scale. A gateway that handles 500 transactions a day smoothly can buckle at 5,000. This is also where the regulatory complexity multiplies. A brand accepting players from Germany, Canada, Brazil, and the Philippines simultaneously needs payment infrastructure that understands each market’s compliance requirements – not one that treats global as a single checkbox. Stage 3: The Maturity Phase (Where the Real Skill Lives) Operators who reach maturity have usually survived at least one payments crisis. They have also made a fundamental mindset shift: payment infrastructure is a strategic asset, not a commodity service. At this level, the conversation shifts from “which gateway is cheapest?” to: What Robust iGaming Payment Solutions Actually Look Like in 2026 The standard has moved significantly in the past two years. Here is what operators serious about longevity now require as baseline: Speed Security Global Compliance This is precisely where working with a high risk payment gateway specialist changes the operational picture entirely. Generic processors are not built for these requirements. Operators who try to force-fit standard merchant infrastructure into high-risk iGaming environments consistently pay for that decision in approval rates, chargeback disputes, and eventually, account terminations. The High-Risk Reality: Why Your Payment Partner Matters More Than Your Platform Here is something most iGaming consultants will not say directly: your gaming platform matters far less than your payments stack. A mediocre game library with exceptional payment flow converts and retains better than an outstanding game library with a clunky, unreliable checkout experience. Players do not tell their friends about your RTP percentages. They do tell their friends when a withdrawal takes four days. Securing a proper merchant account high risk setup – one genuinely built for iGaming transaction profiles – requires working with providers who understand the sector’s nuances: A high risk merchant processing account configured correctly from the start prevents the majority of the crises that destroy iGaming brands in their second and third years. It is not glamorous work. It is the work that keeps the castle standing. Why Operators Who Scale Successfully Think Differently The operators with sustainable, growing iGaming businesses share a common pattern in how they approach iGaming payment solutions: Offshore Gateways works with operators at every stage of this journey – from brands preparing for their first serious volume to established platforms restructuring their processing after a crisis. The pattern is consistent: the operators who treat iGaming payment solutions as a strategic priority outperform those who treat it as a cost to minimise. The Bottom Line Scaling an iGaming brand gets the headlines. Keeping it scaled, keeping approval rates high, chargebacks controlled, players paid on time, and regulators satisfied – that takes genuine operational skill, the right infrastructure, and the right partners. The brutal truth is that most operators learn this too late – after the first major payments disruption has already cost them players, revenue, and processing relationships that took years to build. Ready to build payment infrastructure that scales with your ambition? Talk to Offshore Gateways today and get iGaming payment solutions engineered for operators who are serious about staying at the top. Stay updated on social media as well – Linkedin Frequently Asked Questions What are iGaming payment solutions? These are systems that ensure quick, safe, and international transfers of money from a player to the casino, and vice versa. Why does an iGaming company require a high risk merchant account? Traditional banks consider gambling as a high-risk industry. So, you need a specific type of bank account to cover all the risks associated with betting operations and chargebacks. Is there anything safe about the iGaming payment? Absolutely. All well-reputed companies offer payment solutions, which have both PCI DSS encryption and two-factor authentication to protect sensitive user data. How quick is the withdrawal process when it comes to iGaming payments? The most popular iGaming payment solutions guarantee instant or 24-hour withdrawals to ensure a positive user experience for players. What do I need to know to choose the best iGaming

iGaming Open Banking Challenges & Merchant Solutions

If you run an online gaming or gambling business, you already know the road is never smooth when it comes to getting paid. iGaming businesses face challenges at every turn – from banks refusing accounts to payment providers cutting off services overnight. One of the newest and most promising technologies in the payment world, open banking payments, offers both exciting possibilities and some stubborn obstacles for gaming merchants. In this post, we break it all down in plain language and show you what actually works. What Is Open Banking and Why Does It Matter for iGaming? Open banking for payments is a system that lets customers pay businesses directly from their bank accounts – no credit card, no middleman, no extra fees. Think of it like sending a bank transfer, but faster, smarter, and built into a checkout page. Instead of typing card details, a player logs into their bank app, approves the payment, and the money moves almost instantly. For iGaming operators, this sounds like a dream. Lower fees compared to card processing, instant settlements, fewer chargebacks, and a smoother experience for players. But the reality is a little more complicated. Why iGaming Businesses Face Challenges with Open Banking Payment Providers Even though open banking payment providers are growing fast across Europe, the UK, and beyond, many of them simply will not work with iGaming merchants. Here is why: 1. Heavy Regulatory Scrutiny Online gambling is a licensed, regulated industry – but the rules differ from country to country. Open banking payment providers that serve mainstream retailers often do not want to deal with the compliance burden of gambling licenses, age verification, and anti-money laundering (AML) requirements. So they simply exclude the iGaming category from their terms of service. 2. Bank-Level Blocking Even when an open banking payment solution is technically available, individual banks can block transactions to gambling merchants at the account level. Some banks in the UK and EU have introduced gambling block features that let customers opt in – and those blocks apply to open banking just like they do to cards. 3. High-Risk Labeling and Processing Restrictions iGaming sits firmly in the high-risk category for payment processors. This is not just a credit card problem. High risk payment processing companies — whether they handle cards, bank transfers, or open banking – charge more, have stricter terms, and sometimes close accounts without warning. Open banking is no exception. Many open banking providers apply the same risk logic and turn gaming merchants away. 4. Chargeback and Fraud Concerns Although open banking payment transactions are generally harder to dispute than card payments, fraud and friendly fraud are still concerns. iGaming merchants see players claim transactions were unauthorised after they have lost money, creating headaches for payment providers who would rather avoid the industry altogether. What Does This Actually Mean for Your Business? If you are an iGaming operator trying to offer open banking as a checkout option, you will likely run into walls fast. A standard open banking payment provider will reject your application. A regular merchant center will not approve a gambling merchant account. And your credit card payment terminal setup might be shut down if volumes spike or a processor decides you are too risky. The result? Lost players who wanted a quick, easy deposit method. Higher cart abandonment. Slower growth. Practical Solutions for iGaming Merchants: What Actually Works Here are the most effective ways iGaming operators can get stable, scalable payment processing despite these hurdles: The Role of a Specialist Payment Partner Like Offshoregateways Not every payment gateway can help you. Most are built for low-risk retail merchants who sell physical products or software subscriptions. iGaming is a completely different world — one that demands a partner who understands licensing, jurisdictions, chargebacks, and the specific demands of players who expect frictionless deposits and withdrawals. A good specialist partner brings three things to the table. First, pre-existing relationships with banks and open banking payment providers who actually accept gambling merchants. Second, a diversified acquiring network so that if one processor drops you, another picks up the volume seamlessly. Third, the compliance and risk management infrastructure to keep your accounts healthy long-term. This is exactly the space where Offshoregateways operates. Do Not Let Payment Problems Limit Your Growth The iGaming market is expanding rapidly. Global online gambling revenue is estimated to exceed $100 billion in the next few years, and gamblers are demanding smooth and secure payment processes. This could be through open banking for payment transactions, cryptocurrency acceptance, or localized payment methods for certain regions – your payment system must adapt to this growth. The biggest mistake gaming operators make is treating payment processing as an afterthought. By the time your current provider shuts your account down or your approval rates start falling, it is already too late. The best time to build a robust payment stack is before you need it — not during a crisis. Ready to Solve Your iGaming Payment Challenges? Offshoregateways Can Help If your iGaming business is struggling to get approved for open banking payments, stable card processing, or reliable high-risk merchant accounts – you are not alone, and the problem is solvable. Offshoregateways specialises exclusively in payment solutions for high-risk industries including iGaming, online gambling, sports betting, and fantasy sports. From helping you set up a compliant merchant center account, to sourcing the right open banking payment providers for your specific markets, to building a redundant multi-acquirer stack with chargeback protection – the team at Offshoregateways has the experience and the network to make it happen. Do not let payment friction hold your business back. Contact Offshoregateways today for a free consultation and find out exactly how to build the payment infrastructure your iGaming business deserves. Visit offshoregateways to get started. Stay updated on social media as well – Linkedin Frequently Asked Questions Why do iGaming companies have problems integrating open banking payments? Since banks and gateways treat iGaming as a high-risk segment, most of them simply exclude any gaming merchants due to legal and fraudulent reasons. This regulatory caution makes it difficult

Top Shopify Payment Providers UK: Best Options for High-Risk Merchants

If you run a high-risk Shopify store in the UK, finding a reliable payment gateway is one of the most important decisions you will make. The top Shopify payment providers for high-risk businesses offer flexible underwriting, fast approvals, and solid fraud protection. This guide breaks down the best options for you clearly, so you can start accepting payments without unnecessary delays. Why High-Risk Merchants Struggle With Standard Shopify Payment Gateways Most mainstream providers — including Shopify Payments itself — have strict rules around what businesses they will support. Industries such as jewellery, supplements, adult products, firearms accessories, travel, and subscription boxes are frequently flagged as high-risk. If your store falls into one of these categories, you have likely seen your account frozen or your application rejected. It is frustrating, especially when your business is fully legal and compliant. So, what is the actual solution? Working with a shopify payment gateway uk that specialises in high-risk merchant accounts. These providers understand your industry, assess risk more fairly, and offer better terms over time as your processing history improves. Top Shopify Payment Providers for High-Risk Stores in the UK 1. Offshore Gateways Offshore Gateways is one of the best Shopify payment gateway suppliers in the UK specifically for high-risk merchants. It works with a wide network of acquiring banks across Europe and offshore jurisdictions, which means better approval chances for businesses that traditional providers turn down. Key strengths include multi-currency processing, chargeback management tools, and dedicated account management. For any merchant looking for a Shopify payment gateway UK solution that sticks around long-term, Offshore Gateway is a strong starting point. 2. Stripe (With a High-Risk Workaround) Stripe is widely used as a Shopify payment gateway across the UK. It integrates cleanly with Shopify and supports most currencies. However, Stripe does not directly classify itself as a high-risk processor — meaning accounts in riskier industries face sudden holds. The workaround many merchants use is pairing Stripe with a dedicated high-risk acquiring bank through a payment facilitator. If your business is moderate-risk (not extreme), Stripe can still work — but always have a backup. 3. Worldpay Worldpay is one of the largest Shopify payment gateways UK merchants rely on for high-volume transactions. They serve a broad range of industries and have robust fraud tools. Worldpay’s pricing is not the cheapest, but their stability and uptime record is hard to match. They process over £1 trillion in transactions annually in the UK alone, making them a proven option for serious merchants. 4. PaySafe (Skrill / Neteller Ecosystem) PaySafe and its associated brands are popular across gambling, gaming, and digital goods merchants — sectors that struggle with the best payment gateway for Shopify UK shortlists. Their global reach and multiple-currency payment options make them practical for businesses that sell across borders. 5. Payvision Payvision, now part of ING Group, offers acquiring services for high-risk sectors including nutraceuticals, travel, and online retail. They are a solid pick for UK merchants looking for a stable Shopify payment gateway UK option with European banking relationships. Comparison Table: Top Shopify Payment Providers UK Provider High-Risk Friendly Multi-Currency Chargeback Support Integration with Shopify Offshore Gateways ✅ Yes ✅ Yes ✅ Strong ✅ Full Stripe ⚠️ Limited ✅ Yes ⚠️ Moderate ✅ Native Worldpay ✅ Yes ✅ Yes ✅ Strong ✅ Full PaySafe ✅ Yes ✅ Yes ⚠️ Moderate ✅ Full Payvision ✅ Yes ✅ Yes ✅ Strong ✅ Full What to Look for in a Shopify Payment Gateway UK Chargeback Ratios and Thresholds High-risk merchants must keep chargebacks below 1% (Visa) and 1.5% (Mastercard). If you consistently exceed these thresholds, even the best payment provider for Shopify UK can terminate your account. Look for a gateway that offers real-time chargeback alerts, such as Ethoca or Verifi integrations. Rolling Reserves Many high-risk Shopify payment gateways hold a percentage of your revenue in a rolling reserve — typically 5–10% for 90–180 days. This protects the processor against chargebacks. Negotiate this upfront. Some providers reduce the reserve after 6 months of clean processing history. PCI DSS Compliance All payment gateway in Shopify setups must comply with PCI DSS (Payment Card Industry Data Security Standard). Ask any provider you evaluate whether they are Level 1 PCI compliant. This is non-negotiable if you handle customer card data. Transaction Fees Here is a rough benchmark for the UK market: The best Shopify payment provider UK for your business will not always be the cheapest. Stability, account longevity, and chargeback support are worth paying slightly more for. How to Apply for a High-Risk Shopify Payment Providers UK Account Getting approved is straightforward if you prepare the right documents: The full list of Shopify payment providers in UK that accept high-risk merchants is longer than most people realise. The key is presenting your business professionally and demonstrating a low chargeback history. Choosing From the List of Shopify Payment Providers in the UK The list of shopify payment providers uk merchants should shortlist includes both domestic and offshore acquirers. Don’t limit yourself to providers registered in the UK — offshore acquiring through EU-licensed banks is fully legal, widely used, and often offers better rates for high-risk sectors. Work with a broker or specialist aggregator who has relationships with multiple acquiring banks. This saves time and dramatically improves approval rates. Final Thoughts Choosing the right provider from the top Shopify payment providers available in the UK is not just about processing fees — it is about long-term account stability, chargeback support, and working with a team that understands your industry. If your business has been declined or shut down by mainstream processors, do not assume payment acceptance is out of reach. Specialists like Offshore Gateways exist precisely to support merchants in this situation. Ready to Get Your High-Risk Shopify Payment Providers UK? 📞 Take action today. Visit Offshore Gateways to speak with a payment specialist who understands high-risk Shopify merchants in the UK. Get a tailored quote, compare acquisition options, and start accepting payments within days — not months. Your

Merchant Bank Accounts Explained: Benefits, Setup Process & Requirements

In the current fast-changing digital environment, businesses require an efficient way of receiving payments from customers around the globe. It is at such points that the importance of merchant banking solutions is recognized. Be it an online business, service-based business, or even a high-risk business, understanding the concept of these solutions can help businesses grow at an accelerated pace. This guide is created in such a way that even a beginner can understand the concept of Merchant Bank Accounts in simple terms. What Are Merchant Bank Accounts? A merchant bank account is a special type of account in a bank where a business can receive money from customers using a credit or debit card or other electronic means. When a customer makes a payment to the business, the money will first go to the merchant bank account and then to the main account. A merchant bank account works like a safe box where your customer payments will be kept for a while before they are handed over to you. This ensures your transactions are safe and secure. Merchant bank accounts are a necessity for every business, especially those seeking to expand their businesses and conduct international transactions. Why Are These Accounts Important? All businesses desire easy and secure payment methods. This is because, without the correct system, payments can fail, be delayed, or even be rejected. This is why the correct payment setup is crucial for today’s businesses. These accounts assist businesses in receiving payments from anywhere in the world. They also have security features that help in fraud reduction, thus protecting both the buyer and seller. For high-risk businesses, it is hard to get approval, but the correct company can assist in the process. The next significant advantage is trust. This is because, when customers see secure payment systems, they feel confident in purchasing a product from the business. This will enhance sales and business growth. Benefits of Merchant Bank Accounts One of the biggest advantages of Merchant Bank Accounts is the fact that it allows the business to receive different kinds of payments. For instance, the customers will be able to pay using different cards and even internet banking. This makes the process easy and simple. The accounts also allow businesses to conduct transactions in the most efficient manner. For instance, every payment will be recorded and checked. This makes the process easy and simple. Businesses will also be able to see the amount of money going in and out. The other advantage associated with the Merchant Bank Accounts is the fact that it makes the process secure. For instance, the payment system will be able to use different tools to ensure the process is secure. This will ensure the business and the customers are safe. If the business deals in international transactions, the account will also allow the business to deal in different currencies. How the System Works This process may sound complicated, but it is actually quite simple. When the customer makes the payment, the request goes to the payment gateway. The request then goes to the bank to verify if the payment was valid. If the payment was valid, the money would be held in a special bank account. After a few days, the money would then be transferred to the business owner’s bank account. This ensures that all the transactions are safe and verified before the money is released. Setup Process for Merchant Bank Accounts Setting up the Merchant Bank Accounts is a process that involves a few steps. First, the business will have to find a good and reliable provider that understands the industry and the requirements of the business. After this, the business will have to provide an application with details about the business, including information about the website and the type of services provided. This is then processed by the provider. After this, the account is then connected to a payment gateway. This will allow the business to make transactions. This process takes a few days to a few weeks, depending on the complexity of the business. Finding the right partner is important and can help the business with the process, especially if the business is likely to face problems with approvals. Requirements to Open an Account However, to open such an account, businesses must meet certain conditions. These may vary from one provider to another. Some of the basic conditions may include the business registration status, the presence of a website, and the description of products or services. Businesses may be required to present financial documents to prove the stability of the business. Some providers may ask for the processing history if the business has already handled such services. For high-risk businesses, additional conditions may be required. But working with reliable providers may help in the approval of such accounts. Common Challenges Businesses Face However, many businesses find it difficult to be approved, especially if the business falls in a high-risk industry. Most traditional banks will reject such businesses due to strict policies. Another challenge comes in the form of high fees or long processing times. If a business is not properly set up, it will end up losing customers due to failed or delayed payments. This is where the importance of the right service provider comes in. A good service provider will understand the challenges and offer the best solution to the business. Choosing the Right Partner Not all service providers offer the same quality. However, when choosing a service provider, it is essential to consider experience, reach, and security systems. A good service provider would be able to provide fast approval times, flexibility in terms of payment options, and assistance. They would be able to help businesses comply with regulations. This is where Offshore Gateways excel. They provide services for both regular and high-risk businesses. Final Thoughts It is important that one understands the way these payment processing systems work in order to be able to carry on with their business in the current digital environment. From

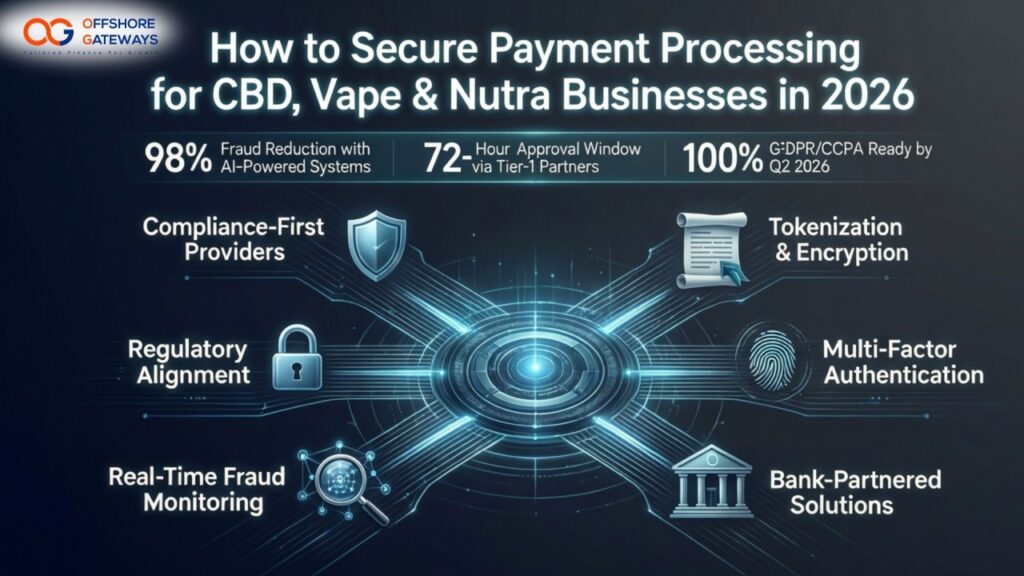

How to Secure Payment Processing for CBD, Vape & Nutra Businesses in 2026

Securing reliable payment infrastructure in the high-risk sector is no longer just about finding a gateway; it is about survival. If you are operating in the hemp, electronic cigarette, or supplement space, you already know the frustration of sudden account freezes and sky-high decline rates. The landscape for CBD Payment Processing 2026 has shifted from basic acceptance to a focus on data-driven stability and multi-rail redundancy. Are you tired of seeing 20% of your legitimate transactions hit a “Do Not Honor” wall? For merchants in 2026, the goal is to move past the “high-risk” stigma and implement systems that mirror the efficiency of low-risk retail. The Reality of CBD Payment Processing 2026 The banking world has not made it easy. Even with widespread legalization, major processors like Stripe or PayPal still frequently ghost hemp-derived product sellers. This is why CBD Payment Processing 2026 requires a specialized merchant account underwritten by banks that actually understand your COAs (Certificates of Analysis) and age-verification workflows. In 2026, the industry has moved toward “Payment Orchestration.” This means instead of relying on one bank, you use a gateway that can route transactions to different acquirers based on the product type or the customer’s location. If one bank tightens its belt, your business keeps running. Why Your Current Account Might Be at Risk Most “instant approval” accounts are actually aggregator accounts. They lump you in with thousands of other merchants. When one “bad apple” in the group gets hit with fraud, the processor might shut down the entire group—including you. True CBD Payment Processing 2026 involves getting your own dedicated Merchant ID (MID). Best CBD-friendly Payment Processors for 2026 Choosing the right partner is the difference between scaling to seven figures and having your funds held for 180 days. Here is a comparison of the top-performing solutions this year: Comparison of High-Risk Payment Solutions Feature Offshore Gateways Typical Aggregators Standard Banks Approval Time 24-48 Hours Instant (then 1-week review) 2-4 Weeks CBD/Vape/Nutra Friendly Yes (Specialized) Limited/Prohibited Usually No Chargeback Tools Integrated Alerts Basic Reporting None Rolling Reserve 5% – 10% None (until a problem starts) N/A Global Reach 100+ Currencies Domestic Only Limited When looking for the Best CBD-friendly payment processors, prioritize those that offer direct U.S. or EU acquiring. Our team at Offshore Gateways specializes in these “hard-to-place” accounts, ensuring you get the longevity your brand deserves. Instant Approvals for Vape and E-Cigarette Merchants If you are in the vape industry, you face the PACT Act and strict age-gating requirements. Getting a vape merchant account instant approval is possible, but it comes with a caveat: your website must be 100% compliant before you hit “apply.” Underwriters in 2026 are looking for: A vape merchant account instant approval should not mean “no questions asked.” It should mean a streamlined digital application where your documents are verified by AI in real-time, getting you live in hours, not weeks. Nutra Subscription Payment Processing: Ending the “Trial” Nightmare Nutraceuticals are the kings of the subscription model, but they are also the kings of “friendly fraud.” Customers often forget they signed up for a monthly supply of Vitamin K or Keto gummies and hit the “dispute” button rather than “cancel.” For nutra subscription payment processing, 2026 is all about transparency. To keep your merchant account healthy, you need: Are you monitoring your “descriptor” on customer bank statements? If your website is “PureHealth.com” but the charge says “PH-Services LLC,” you are asking for a chargeback. Integrating Non-Prohibitive CBD Gateways Many merchants make the mistake of choosing a platform like Shopify or WooCommerce and then realizing the default payment settings prohibit hemp products. You need non-prohibitive CBD gateways for Shopify/WooCommerce that plug in via API. In 2026, the Best CBD-friendly payment processors provide native integrations. This means your customer never leaves your site to complete a payment. Redirection is a conversion killer. By using a specialized gateway, you can manage CBD payment processing 2026 directly within your existing dashboard. Pro Tip: Always have a “Plan B” gateway configured. If your primary gateway has a technical hiccup, your “Plan B” should automatically take over the traffic. The Science of Chargeback Mitigation for High-Risk E-commerce In the high-risk world, a chargeback ratio over 1% can get you terminated. This is why chargeback mitigation for high-risk e-commerce is now a mandatory part of your tech stack. Tools like Verifi and Ethoca allow you to “pause” a dispute before it becomes a chargeback. You get an alert, you refund the customer immediately, and the bank never counts it as a strike against your account. It costs a small fee, but compared to losing your entire CBD Payment Processing 2026 infrastructure, it is a bargain. Steps to Lower Your Risk Profile: Why 2026 is the Year of “Evidence-Based” Processing Gone are the days of “gray market” processing where you hide your products behind a shell company. In CBD Payment Processing 2026, honesty is the only way to scale. Banks are using automated crawlers to scan your site daily for prohibited claims (e.g., “This CBD cures cancer”). If your site is clean and your documents are ready, you can access low-rate high-risk processing 2026 tiers that were previously reserved for big-box retailers. Is your documentation up to date? Conclusion: Securing Your Future in High-Risk Retail The world of CBD Payment Processing 2026 is more stable than ever for those who play by the rules. By choosing the Best CBD-friendly payment processors and implementing chargeback mitigation for high-risk e-commerce, you protect your cash flow from the whims of traditional banking. Don’t wait for a “Notice of Termination” to find a better partner. Whether you need a vape merchant account instant approval or a stable home for nutra subscription payment processing, the time to diversify your payment rails is now.

7 Reasons Why Global Businesses Are Moving to Offshore Payment Solutions

Have you ever had a legitimate international transaction declined for no clear reason? Or watched a customer abandon their cart because your payment gateway doesn’t support their currency? These are real problems that cost businesses millions every year and they’re pushing smart entrepreneurs toward offshore payment solutions faster than ever before. Offshore payment solutions are no longer just for high-risk industries or large multinationals. Small and mid-sized businesses across India and the world are making the switch because the benefits are simply too good to ignore. Whether you’re selling software subscriptions, running an e-commerce store, or offering financial services, the right offshore payment gateway can completely transform how money flows through your business. This guide breaks down exactly why global businesses are making this move and what it means for you. What Are Offshore Payment Solutions, Really? Let’s clear up a common misconception. Offshore payment solutions are not about hiding money or dodging taxes. They are legitimate financial tools that allow businesses to accept payments through banks or processors registered in a different country than where the business operates. A simple example: an Indian digital marketing agency might use an offshore merchant account registered in the UK or Cyprus to accept payments from US and European clients. This gives them access to multi-currency billing, lower interchange fees, and fewer restrictions compared to domestic processors. International payment processing through offshore channels often comes with greater flexibility in which industries are served, which payment methods are accepted, and what currencies can be processed. Think of it as upgrading from a local taxi to a full international ride network. Why Businesses Are Making the Switch: 7 Reasons 1. Access to High-Risk Industry Support Many domestic banks and payment processors automatically reject businesses in industries they classify as “high-risk”-including online gaming, Forex, nutraceuticals, travel, adult entertainment, and even some subscription-based SaaS companies. If your business falls into one of these categories, a high-risk payment gateway offered through offshore channels may be your only viable option for smooth, uninterrupted processing. A Forex trading platform based in Mumbai, for example, will find it nearly impossible to get reliable domestic processing. By partnering with an offshore payment gateway provider, they can secure stable processing, handle chargebacks more efficiently, and keep their cash flow intact. 2. Multi-Currency Payment Capabilities Does your business accept payments in USD, EUR, GBP, AED, or AUD? If you’re relying on a standard domestic gateway, you’re likely paying steep conversion fees and losing customers who prefer to pay in their local currency. Multi-currency payment gateway solutions-a core feature of most offshore payment solutions allow you to display prices and accept payments in dozens of currencies simultaneously. This reduces cart abandonment, builds trust with international customers, and eliminates the confusion of forced currency conversions. 3. Lower Transaction Fees and Better Rates This one surprises many business owners. Offshore payment processors often offer significantly lower transaction fees than domestic alternatives-especially for cross-border transactions. Because they operate in jurisdictions with favorable financial regulations, they can pass those savings on to merchants. For a business processing $100,000 per month in international transactions, even a 0.5% reduction in fees saves $6,000 per year. Scale that up and you’re looking at a very real competitive advantage. 4. Fewer Restrictions, More Approvals Domestic banks often impose strict merchant category codes (MCCs) that determine what kind of business you can run and how much volume you can process. Cross-border payment solutions offered by offshore providers typically come with far greater flexibility. Many businesses report that their international approval rates jump dramatically after switching to offshore payment solutions-in some cases from 60% to over 90%. For e-commerce businesses especially, that difference in approval rate directly translates to revenue. 5. Better Chargeback Management Chargebacks are the silent killer of online businesses. A high chargeback ratio can get your account terminated by a domestic processor with very little warning. Offshore payment solutions are often better equipped to handle chargeback-heavy industries, offering dedicated risk management tools, chargeback alerts, and dispute resolution support. This is particularly relevant for Indian businesses selling internationally, where disputes can arise from time zone differences, language barriers, or varying consumer protection laws. 6. Geographic Redundancy and Uptime What happens when your payment processor goes down? For most businesses using a single domestic gateway, the answer is: you stop making money. Global payment processing solutions through offshore providers typically offer redundant systems across multiple geographies, dramatically reducing downtime and ensuring that payments keep flowing even if one system experiences issues. 7. Financial Privacy and Asset Protection Legitimate businesses operating in politically or economically volatile regions often seek offshore banking solutions as a form of financial protection. This is about legal risk management ensuring that business funds aren’t frozen or disrupted by local regulatory changes or banking crises. Countries like Cyprus, Malta, Seychelles, and the Cayman Islands offer stable financial environments that many businesses find attractive for this reason. Who Benefits Most from Offshore Payment Solutions? Not every business needs to go offshore but for many, it’s the single most impactful decision they can make for their payment infrastructure. Here’s a quick breakdown of who benefits most: E-commerce Businesses selling across multiple countries need multi-currency support and high approval rates. Offshore solutions deliver both. An Indian Shopify merchant selling to customers in the US, UK, and Australia can consolidate their international payment processing into a single, efficient offshore gateway. SaaS Companies and Subscription Businesses dealing with recurring billing, free trials, and subscription cancellations face a higher-than-average chargeback risk. A well-configured offshore payment gateway with recurring billing tools is designed exactly for this use case. Travel and Hospitality Businesses are considered high-risk by most domestic processors due to advance bookings and high cancellation rates. Cross-border transaction solutions tailored for the travel industry make processing seamless. Forex and Crypto Platforms face the most restrictions domestically and have the most to gain from offshore processing. For these businesses, offshore payment solutions are essentially non-negotiable. Common Questions About Offshore Payment Solutions Are offshore payment solutions legal in